After six consecutive quarters of declining shipments, the smartphone market share is in bad health, but according to Canalys, there is light at the end of the tunnel as analysts have already begun to notice signs of recovery.

Even with the slight improvement above the 12% fall in Q1, global smartphone shipments still declined 11% year over year. Vendors are attempting to move out older models to accommodate new launches. Therefore, inventory is decreasing. A supply of essential components is also something they are working to guarantee as insurance against a sudden price increase.

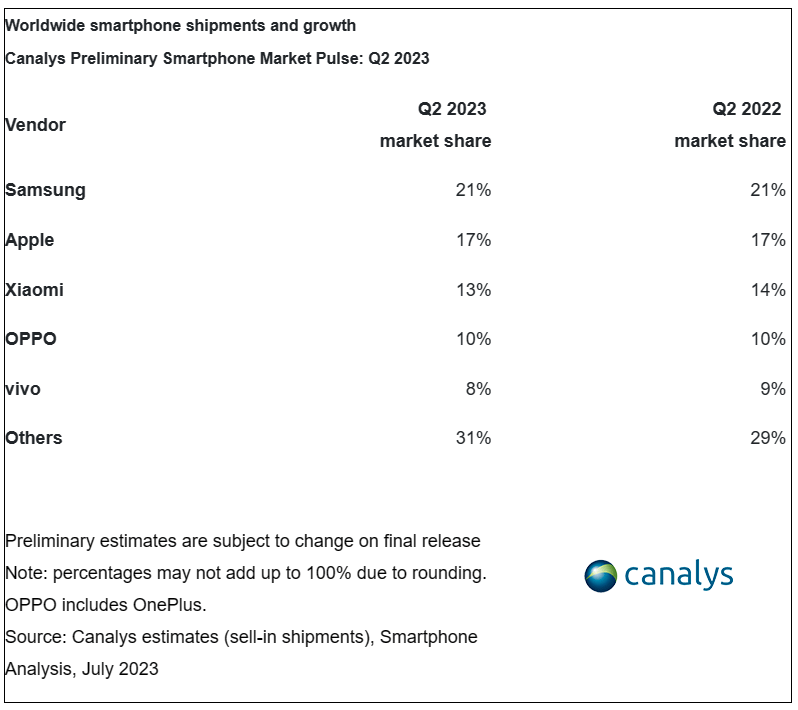

The Top 5 smartphone manufacturers kept their rankings from the prior quarter, albeit some fell more than others (Apple fell from 21% in Q1 to 17% in Q2, while Samsung remained comparatively consistent, falling from 22% to 21%).

On the strength of the robust demand for new Redmi models, Xiaomi increased by two percentage points. Similarly, the inexpensive Y-series from Vivo is proving to be very popular. In the Asia-Pacific area, Oppo and OnePlus are doing well in their primary markets. Notably, Canalys follows Vivo individually but mixes the data from Oppo and OnePlus.

According to Le Xuan Chiew, an Analyst at Canalys, “Oppo, vivo, Transsion, and Xiaomi are increasing their smartphone market share in the sub-$200 price band through stronger sales incentives and retail aggression.” It’s not just them. According to Canalys, “growing channel investments in the form of channel incentives and targeted marketing campaigns to stimulate consumer demand for new launches, driving channel activity” have been made.